The United States rushed to seize the assets of Silicon Valley Bank on Friday after it experienced a run on the bank.

Silicon Valley, the nation's 16th-largest bank, failed after depositors — mostly technology workers and venture capital-backed companies — hurried to withdraw money this week as anxiety over the bank's balance sheet spread. It is the second biggest bank failure in U.S. history, behind Washington Mutual during the height of the financial crisis more than a decade ago.

Silicon Valley was heavily exposed to the tech industry and there is little chance of contagion in the banking sector similar to the chaos in the months leading up to the Great Recession more than a decade ago. The biggest banks — those most likely to cause a systemic economic issue — have healthy balance sheets and plenty of capital.

In 2007, the biggest financial crisis since the Great Depression rippled across the globe after mortgage-backed securities tied to ill-advised housing loans rippled from the United States to Asia and Europe. The panic on Wall Street led to the collapse of the storied Lehman Brothers, founded in 1847. Because major banks had extensive exposure to one another, it led to cascading disruption throughout the global financial system, putting millions out of work.

A sign posted on a Silicon Valley Bank in Santa Clara, California, March 10, 2023.

There has been unease in the banking sector all week and the collapse of Silicon Valley pushed shares of almost all financial institutions lower Friday, shares that had already tumbled by double digits since Monday.

Silicon Valley Bank's failure arrived with incredible speed, with some industry analysts on Friday suggesting it was a good company and still likely a wise investment. Silicon Valley Bank executives were trying to raise capital early Friday and find additional investors. However, trading in the bank's shares was halted before the opening bell on Wall Street because of extreme volatility.

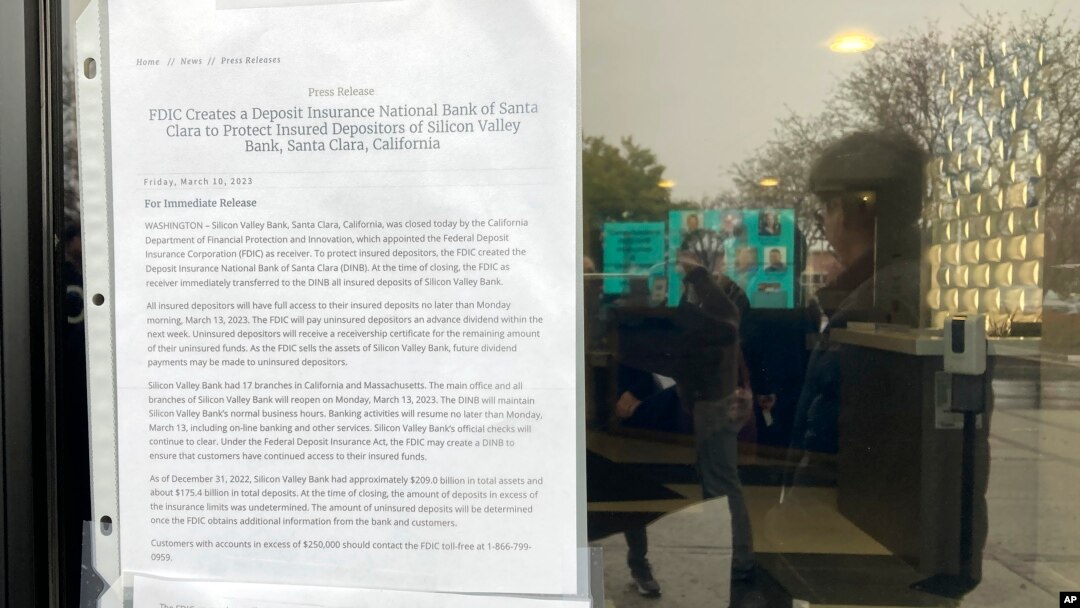

Shortly before noon eastern, the Federal Deposit Insurance Corporation moved to shutter the bank. Notably, the FDIC did not wait until the close of business to seize the bank, as is typical in an orderly wind down of a financial institution. The FDIC could not immediately find a buyer for the bank's assets, signaling how fast depositors had cashed out. The bank's remaining uninsured deposits will now be locked up in receivership.

The bank had $209 billion in total assets at the time of failure, the FDIC said. It was unclear how much of its deposits were above the $250,000 insurance limit at the moment, but previous regulatory reports showed that much of Silicon Valley Bank's deposits exceeded that limit.

The FDIC said Friday that deposits below the $250,000 limit would be available Monday morning.

Silicon Valley Bank appeared stable this year, but on Thursday it announced plans to raise up to $1.75 billion to strengthen its capital position. That sent investors scurrying and shares plunged 60%. They fell further on Friday before the opening of the Nasdaq, where it is traded.

A person standing in an entrance of a Silicon Valley Bank, middle rear, talks to people waiting outside the bank in Santa Clara, California, March 10, 2023.

As its name implied, Silicon Valley Bank was a major financial conduit between the technology sector, its founders and startups as well as its workers. Hundreds of companies held their operating capital with the bank, and it was seen as good business sense to develop a relationship with Silicon Valley Bank if a founder wanted to find new investors or go public.

"We saw building a relationship with Silicon Valley Bank as a logical step, given their reach," said Ashley Tyrner, CEO of FarmboxRx, a company that delivers food as medicine to Medicaid and Medicare recipients. While Tyrner has money in other banks and can make payroll, she said a good portion of her business' profits are now locked up with the bank.

Silicon Valley's connections to the tech sector became a liability rapidly. Technology stocks have been hit hard in the past 18 months after a growth surge during the pandemic and layoffs have spread throughout the industry.

At the same time, the bank was hit hard by the Federal Reserve's fight against inflation and an aggressive series of interest rate hikes to cool the economy.

As the Fed raises its benchmark interest rate, the value of bonds, typically a stable asset, start to fall. That is not typically a problem as the declines lead to "unrealized losses," or losses that are not counted against them when calculating the capital cushion than banks can use should there be a downturn in the future.

However, when depositors grow anxious and begin withdrawing their money, banks sometimes have to sell those bonds before they mature to cover that exodus.

That is exactly what happened to Silicon Valley Bank, which had to sell $21 billion in highly liquid assets to cover the exodus of deposits. It took a $1.8 billion loss on that sale.

Tyrner said she's spoken to several friends who are backed by venture capital. She described those friends as being "beside themselves" over the bank's failure. Tyrner's chief operating officer tried to withdraw her company's funds on Thursday but failed to do so in time.

"One friend said they couldn't make payroll today and cried when they had to inform 200 employees because of this issue," Tyrner said.